By Stephen Applebaum and Alan Demers —

As we dwell in an period of technological growth, it’s more and more troublesome to separate hype from actuality. With so many breakthroughs in drugs, house exploration and even autonomous driving, it’s not advisable to guess in opposition to even the boldest of efforts. So, maybe people will certainly dwell on Mars someday. In current occasions, the nay-saying in opposition to hype is mostly about when it should occur, and fewer about if it should occur.

The P&C insurance coverage house has seen its share of hyped ideas, together with blockchain and digital actuality, however none matched the current exuberance for AI – and for good motive. Insurance coverage practices are all about info gathering and validation, whether or not for underwriting, claims or danger administration. Actuarial mathematical sciences are utilized for trending and pricing. And a number of different inside capabilities and exterior processes are only a few methods to explain insurance coverage at-a-glance. All of which can profit from AI instruments and brokers near-term and into the long run. Insurance coverage expertise shortages, excessive prices of insurance coverage for customers and companies, altering dangers, demand for loss prediction and prevention are simply a number of the greater challenges during which AI might come to the rescue.

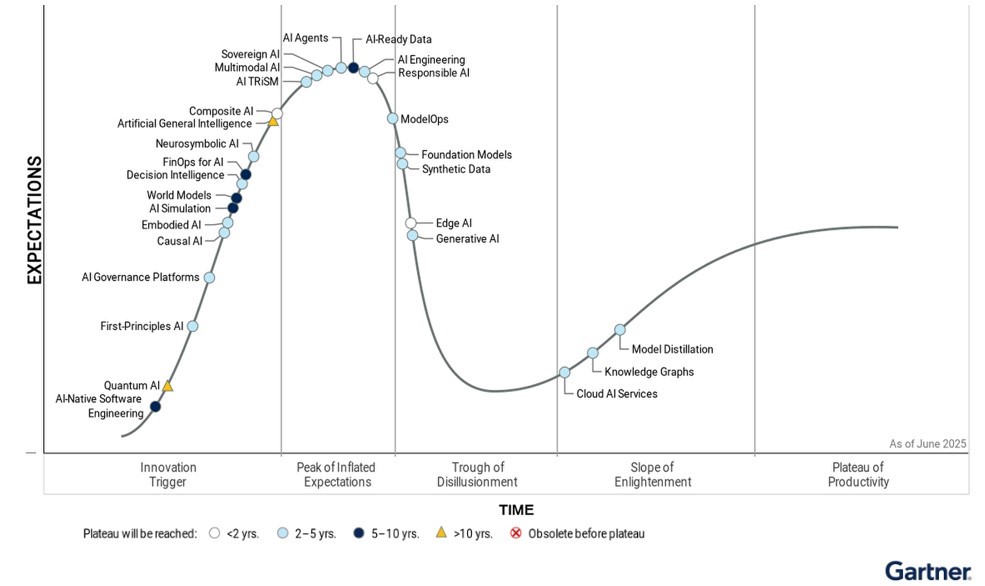

The Gartner Hype Cycle

Most of us are accustomed to The Gartner Hype Cycle, a visible mannequin that illustrates the maturity, adoption, and social software of a brand new know-how, charting its development via 5 key phases. It supplies a framework to information know-how investments by displaying when a know-how’s precise worth turns into clearer, serving to organizations cut back dangers and make knowledgeable choices about when to undertake rising applied sciences. As priceless because it has been, the arrival of AI applied sciences might problem its relevancy.

References to AI and associated software are unimaginable to keep away from which may lead many people to conclude that we now have moved from The Peak of Inflated Expectations and are approaching the dreaded Trough of Disillusionment within the Gartner Hype Cycle (see beneath).

Certainly, Edge AI and Generative AI has simply barely entered this section in Gartner’s 2025 report:

Nevertheless, it’s our rivalry that many different makes use of of AI – together with AI Brokers and Determination Intelligence, in insurance coverage and past – may defy the historical past of latest applied sciences and collapse the mannequin, skipping proper over and/or compressing the trough and transferring straight on to The Slope of Enlightenment and The Plateau of Productiveness.

This isn’t to say that AI adoption – we may name it commercialization at scale – shouldn’t be with out loads of headwinds. Regulators are lawmakers are expressing moral and information privateness issues. Labor unions, service, and data staff are involved about employment safety. Insurance coverage provider adoption for all new know-how is commonly fairly gradual and when it comes to years with AI demonstrating the very best scrutiny ever. Information privateness, authorized publicity and model safety are entrance of thoughts amongst insurers. As official as these issues could also be, collectively they underscore the large potential for disruption that these applied sciences characterize.

AI in Insurance coverage

The insurance coverage trade is among the many earliest adopters of AI, though the use circumstances are nonetheless considerably fundamental and never but delivering materials returns. However we warning carriers to not permit these early experiences to discourage higher funding and analysis – the potential returns can’t be ignored and furthermore neither can the aggressive market benefits.

Worldwide Insurance coverage Society Report Identifies the Speedy Rise of Synthetic Intelligence

The Worldwide Insurance coverage Society is affiliated with The Institutes. The IIS collaborated with The Institutes to conduct this survey, together with a number of associates. These embody the Insurance coverage Data Institute, Insurance coverage Thought Management, and Pacific Insurance coverage Convention.

Based on their newest report, in 2025, synthetic intelligence (AI) has emerged because the single most vital precedence amongst trade executives, surpassing inflation for the primary time lately. Two-thirds of executives now place AI on the high of their know-how and innovation agendas, representing a gradual climb from simply 17% in 2021. This accelerated focus is pushed by the rising realization that AI can streamline operations, improve information analytics, and open new avenues for product innovation, all of that are seen as crucial for staying aggressive in an evolving enterprise panorama.

One government described the advantages of AI to their backside line: “These instruments improve forecasting capabilities by permitting for deeper insights into traits and potential future dangers. By empowering themselves with sturdy analytics, organizations can enhance their strategic planning and danger administration efforts, finally driving higher enterprise outcomes.”

P&C Observations on AI Adoption

The next is a snapshot of what we’re seeing and listening to at the moment from carriers and others:

- Insurers are embracing the ideas of AI to learn in a number of areas together with danger choice, underwriting, operational effectivity, and value administration amongst different areas. Claims, Underwriting are usually essentially the most usually cited insurance coverage use areas

- C-Suites actively selling and setting mandates to advance AI agendas with a “let’s not get left behind” mantra

- The variability and variety of use circumstances for almost each insurance coverage operate from product growth to distribution and repair are outstanding and optimistic

- Inside insurance coverage provider Governance Panels have a tendency slender, halt and maybe appropriately stall growth of use circumstances because of information safety and privateness, authorized, and reputational hurt dangers together with anticipated future regulatory controls

- AI for insurance coverage encompasses a variety of varieties and utilization from pc imaginative and prescient, generative, conversational (chatbots), agentic, predictive and extra

- Doc evaluate and summarization is a selected and in style use, e.g., medical data, demand packages, authorized paperwork

- Different areas of use embody danger part, CAT modeling, declare case escalation, visible harm analysis instruments, reserving, insurance coverage gross sales, and quite a few inside processing capabilities

- Carriers are combined when it comes to purchase vs construct with most doing each by partnering with AI options corporations and constructing proprietary options

- There’s an abundance of “AI answer” suppliers with .ai of their url or in any other case in advertising materials making it extraordinarily troublesome to tell apart

- Insurers are extremely protecting when contracting with distributors and suppliers, centered on information safety and privateness and buckle down on AI utilization, information entry and associated gadgets

- Demand on folks together with AI information, expertise and capabilities are understated with regards to change administration

Regulators and AI

The Nationwide Affiliation of Insurance coverage Commissioners (NAIC) has launched mannequin steerage and laws for the usage of Synthetic Intelligence Techniques by Insurers which have been adopted by 24 states (see NAIC Mannequin and NAIC Mannequin Adoption Map).

Customers and AI

The April 2025 Genpact Client AI Examine reveals {that a} majority (55%) of US grownup respondents really feel impartial about their insurance coverage corporations utilizing AI, and 25% view it negatively. Nevertheless, when AI delivers tangible advantages – resembling quicker and extra correct claims processing, custom-made quotes, and improved customer support – buyer acceptance will increase considerably. The findings emphasize a chance for insurers to shift notion and construct desire and belief with their prospects.

“As insurers embrace AI to boost operations or buyer expertise, they have to be sure that each interplay – whether or not human-led or AI-powered – meets or exceeds buyer expectations,” mentioned Adil Ilyas, International Enterprise Chief for Insurance coverage at Genpact. “This analysis highlights AI’s potential to rework insurance coverage, but additionally the necessity for insurers to shut expertise gaps and talk transparently to construct belief and loyalty.”

Suggestions for P&C Trade Leaders

Prioritize governance and mannequin danger administration now. Regulators and plaintiffs are centered right here — being proactive protects each prospects and the steadiness sheet.

Focus first on high-value, low-risk gen-AI deployments (inside productiveness, doc summarization, FNOL help) whereas constructing the info and MLOps spine.

Deal with distributors and basis fashions as focus danger — strengthen contractual, privateness and incident response clauses.

Measure outcomes, not simply outputs — monitor bias metrics, enchantment reversal charges, buyer satisfaction and monetary KPIs

Plan for regulatory change — assume extra granular supervisory questions and state/federal enforcement within the quick time period.

Disclosure and Transparency

We employed ChatGPT to collect a number of the info for this text which itself is validation of our premise that AI is turning into pervasive and is simply too priceless to disregard for sure duties. We consider that any printed work ought to incude an AI disclosure assertion. When used along side the creator’s personal expertise, knowledgeable insights, widespread sense, and moral judgement it appears like AI may assist make it an thrilling future.

Though insurance coverage AI hype exceeds measurable uplift in the intervening time, it’s our view that AI isn’t just one other know-how bubble. AI in insurance coverage holds super potential to finally clear up the numerous worsening gaps and challenges within the insurance coverage mannequin.

Ready for regulatory readability or delaying to fully de-risk AI might show to be a detrimental path with first movers having an insurmountable benefit.

In regards to the Authors

Stephen E. Applebaum, Managing Associate, Insurance coverage Options Group, is a topic skilled and thought chief offering consulting, advisory, analysis and strategic M&A companies to contributors throughout all the North American property/casualty insurance coverage ecosystem centered on insurance coverage info know-how, claims, innovation, disruption, provide chain, vendor and efficiency administration. Mr. Applebaum can also be a Senior Advisor to Waller Helms Advisors. WHA is the premier funding banking boutique centered on the crossroads of the Insurance coverage, Healthcare and Funding Companies sectors.

Stephen is a frequent chairman, visitor speaker and panelist at insurance coverage trade conferences and contributor to main insurance coverage trade publications and has a ardour for teaching, mentoring, enterprise course of innovation and constructive transformation, making use of disruptive know-how, and managing organizational change within the North American property/casualty insurance coverage trade and buying and selling companion communities. He could be reached at Stephen.Applebaum@gmail.com.

Alan Demers is founder and president of InsurTech Consulting LLC, with 30 years of P&C insurance coverage claims expertise, offering consultative companies centered on innovating claims. After initiating and main claims innovation at Nationwide, Demers collaborates within the forefront of InsurTech, partnering with insurance coverage leaders, startups, design pondering consultants and repair suppliers to modernize private, industrial and specialty claims.

As Vice President of Claims Innovation at Nationwide, Alan conceptualized a imaginative and prescient and highway map to construct next-generation claims, automating and digitizing claims experiences, progressing from inception via prototype testing. He served as a founding member of the Company Innovation Council and performed a key management function in establishing targets, practices and an revolutionary tradition at Nationwide.

Alan is an achieved government chief and has labored for 2 separate Fortune 100 insurance coverage corporations in numerous company, nationwide and regional management roles amongst private, industrial, non-standard and specialty strains claims. Previous to main claims innovation, he served as head of claims for Nationwide’s industrial agribusiness and non-standard claims. Different noteworthy roles embody: subject vice chairman, regional claims officer and nationwide disaster director, high quality assurance director.

Alan started his profession with Aetna as a declare adjuster and superior to a company declare guide, previous to becoming a member of Nationwide in 1995.